Step 2. Learn about the post clearance audit methodology and how it can assist trade facilitation and control.

Post clearance audit

Definition/Scope

Post clearance audit (PCA) or audit-based controls are defined by the Revised Kyoto Convention as measures by which the Customs satisfy themselves as to the accuracy and authenticity of declarations through the examination of the relevant books, records, business systems and commercial data held by persons concerned. Post-clearance audit is a critical control methodology for Customs and other border regulatory authorities as it enables them to apply a multi-layered risk-based control approach by moving from a strictly transaction-based control environment to a stronger audit-based administration. Transaction-based controls are those controls applied to each individual shipment at the time of crossing the border, such as physical examination, verification of value, origin and classification of goods, sampling, verification of certificates, licences and permits, etc.

Problem statement

Administrations that do not use audit-based controls usually concentrate their controls entirely at the border and at the time of import, and often apply a 100 % physical examination approach. This leads not only to unnecessarily long delays at the border but is also a very ineffective and inefficient use of the limited control and inspection staff at the border. In addition, 100% physical examiniation creates an enabling environment for corrupt practices. Audit-based controls are a prerequisite for administrations to successfully apply other trade facilitation measures, such as segregation of release and clearance, simplified procedures for authorized traders and AEOs or the WTO valuation rules.

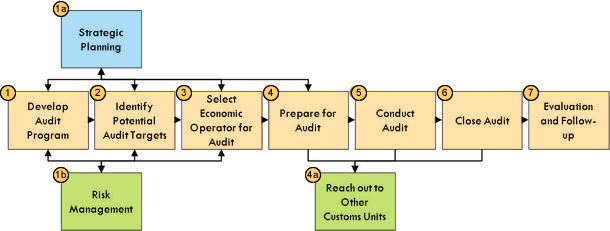

Implementation guidance

Post-clearance audit allows reduction of control activities at a border and at the time of arrival of goods to only those necessary to determine the admissibility of the goods. This can lead to a significant increase in revenue collection, as PCA allows a more comprehensive and holistic evaluation of the particulars necessary for the calculation of duties and taxes. In Japan, for example, the increased use of PCA generated more than twice as much revenue in 2009 than in 1999.

PCA can have the form of supporting transaction-based controls at the border by verifying the classification, valuation and origin of the goods after release through an audit of the supporting commercial documentation such as an invoice. In this way, goods can be released upon arrival (usually against security or guarantee) and clearance be completed and duties paid after the PCA. This segregation of release and clearance is a very important measure to accelerate the movement of goods across borders. Modern Customs administrations may be in a position to grant release and clearance simultaneously upon arrival of the goods, as stipulated in the ICC Customs Guideline # 9.

In addition, PCA can have the form of periodic and cyclic audits, usually at the premises of the importer or trader concerned, where Customs reviews imports over a given period and checks all relevant commercial records, including bank statements and contracts to verify the particulars given in a goods declaration. Both forms of PCA should be performed following a risk-based selectivity approach similar to that applied to individual transactions at the time of import or export.

PCA requires an enabling environment such as a dedicated PCA organization within Customs, the legal powers to access commercial records and to enter traders’ premises, properly trained staff, as well as the existence and proper application of accounting standards (e.g. based on the International Financial Reporting Standards (IFRS) as adopted by the International Accounting Standards Board) based on which companies keep their records. Only by following such accounting standards will Customs be in a position to introduce audit-based controls.

Additional information (references, examples, etc.)

The ICC Customs Guideline # 19 provide additional aspects from a business perspective. The WCO Guidelines to Chapter 6 of the Revised Kyoto Convention as well as the WCO Guidelines For Post-Clearance Audit (March 2006) provide detailed information on how to set up an audit-based control process and establish the supporting institutional framework in terms of organization and regulations, including the legal powers necessary for PCA. These WCO guidelines are not freely available.