Reverse factoring

Reverse factoring (i.e. approved payables financing) allows sellers to sell their receivables and/or drafts relating to a particular buyer to a bank at a discount as soon as they are approved by the buyer. This allows the buyer to pay at the normal invoice/draft due date and the seller to receive early payment. The bank relies on the credit worthiness of the buyer so the cost of capital applied to the supplier is based on an arbitrage between the lower cost of capital of the buyer and the higher cost of the supplier.

Implementation guidance

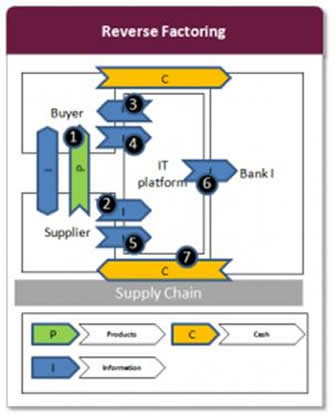

The starting point for reverse factoring is an approved invoice. A schematic view of the reverse factoring process is shown below.

- The basis for the construction is the underlying transaction between the buyer and supplier.

- Subsequently the invoice for this transaction is submitted through the IT platform by the supplier.

- This enables the buying party’s information system to receive it .

- As soon as the buyer has approved the invoice, it is communicated via the platform, allowing the supplier to see it.

- It is up to the supplier to either wait until the payment term expires and the buyer pays the invoice, or to request a credit grant from the bank.

- The bank receives this request via the IT platform.

- The bank pays the supplier for the invoices, withholding the agreed fees. When the agreed payment term expires, the buyer makes a payment to the bank, after which all obligations have been met. The finance risk of the bank is transferred from the bank-supplier to the bank-buyer because the approval of the invoice by the buyer forms the basis for the decision of the bank to grant credit.

In Spanish-speaking countries this instrument is known as “Confirming”.